The gold exploration and development company's assets are located in the West African country and include the Bolgatanga and Subranum projects - and the flagship, 7 million ounce Namdini which has a 15-year mining licence in place, environmental permitting and studies underway.

"Cardinal provides investors with exposure to potential world-class developing gold assets located in Ghana, a politically stable country which supports and welcomes mining activities," managing director and CEO Archie Koimtsidis says.

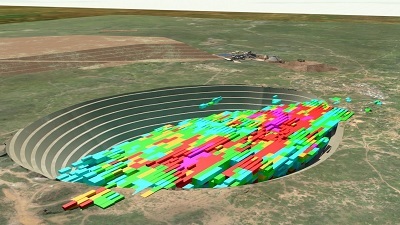

Namdini is being methodically de-risked by Cardinal's highly experienced management team, as the company works to develop a gold mine at the large-scale, shallow deposit that spans more than 1km and remains open along strike and at depth.

The company's aggressive drilling programme has yielded impressive results for Namdini, which now comprises an indicated 6.5Moz Au and 0.5Moz Au inferred resource, and the company anticipates a positive conversion of resources in an upcoming maiden reserve estimate.

A robust preliminary economic assessment earlier this year outlined three positive, prospective development options - 4.5 million tonne per annum, 7Mtpa and 9.5Mtpa - which are being finetuned in a preliminary feasibility study due this quarter.

"Preliminary studies for a larger throughput option in terms of return on capital and NPV evaluation are ongoing," Koimtsidis said.

The company is on track to release a PFS in Q3

A higher grade, low-strip starter pit scenario, which could dramatically reduce the payback period for the large-scale development project, has also been identified.

Meanwhile, metallurgical testwork optimisation is ongoing with a series of variability tests being added to the starter pit and life of mine initial tests, and will be ready in time to support the PFS.

The PFS, and the subsequent definitive feasibility study which is expected to be completed in about 12 months' time, are set to be funded through a US$25 million senior secured credit facility with Sprott Private Resource Lending, which was being finalised at the time of going to print.

"This is significant to Cardinal as it shows third party validation and support from a leading industry participant, who is already an existing shareholder," Koimtsidis said.

"This facility provides Cardinal with the ability to continue to fast track Namdini towards completion of a definitive feasibility study in Q3 2019, while maximising shareholder value by avoiding unnecessary dilution."

The company also has attracted investor backing from miner Gold Fields (Australia) and institutions including Van Eck.

Koimtsidis reiterated Cardinal's belief it will outperform its peer group over the next year, given the positive outcomes of the PEA, the expected maiden mineral ore reserve and anticipated positive PFS.

The company has recently benchmarked itself against peers in terms of market capitalisation, price to net asset value and enterprise value per resource ounce and says the exercise shows Cardinal represents a significant investment opportunity.

"Cardinal's market capitalisation as a gold exploration company going into project development continues to show strong market support for our projects, in particular the Namdini Gold Project, which is showing high economic return potential," Koimtsidis said.

"The price to net asset value (P/NAV) for Cardinal's Namdini different throughput options indicates the attractive value for shareholders for the project."

He said P/NAV was an extremely important mining valuation metric, NAV being the net present value (NPV) or discounted cash flow (DCF) value of all the future cash flow of the mining asset less any debt plus any cash.

"Our current P/NAV shows that we are undervalued against our peers hence the investment opportunity," he said.

As for the third metric, Koimtsidis said the enterprise value per resource ounce considered the total resources contained in the ground and divided it by the enterprise value of the business, again showing Cardinal offered "huge potential for its world class deposit which stands at 7Moz against a current substantial enterprise value".

Cardinal Resources CEO and MD Archie Koimtsidis

Koimtsidis is also especially proud of Cardinal's low discovery cost per ounce.

"Cardinal is a market leader in gold discovery costs at a remarkable US$6 per ounce, as compared to an industry average of $147," he told MNN.

Beyond Namdini, Cardinal has recently demonstrated further exploration success with last month's new gold discovery, dubbed Ndongo East, on its Ndongo licence 15km north of Namdini.

First pass RC drilling highlights included 9m at 23.3g/t from 60m and rock chip samples returned significant grades including 13.7g/t.

Koimtsidis said exploration was continuing in earnest on the Bolgatanga project tenements in Ghana's north.

"Although our primary strategy is to find another large deposit like Namdini, identifying high grade satellite deposits that are close enough to be trucked to Namdini are also being targeted," he said.

"Auger drill soil sampling (gold and indicator elements), geological mapping, geophysical surveys such as magnetics, IP and gravity, followed up by scout RC drilling, are some of the methods being applied."

The company also has the 69km² Subranum project in southwest Ghana that straddles the eastern margin of the Sefwi gold belt.

"The Sefwi Belt is highly prospective and is spatially related to major discoveries including the 7Moz Bibiani Gold Mine (approximately 70 km southwest), Newmont's Ahafo 23Moz gold mine (approximately 53 km west) and Kinross' Chirano 5Moz gold mine (approximately 110km southwest)," he said.

He pointed out Ghana was home to several junior, intermediate and large mining companies and said the country had an established mining and tax regime in place that provided a clear framework for advancing projects.

"Cardinal Resources has attracted and maintained strong investment support, as its Namdini Gold Project located in the northern region of Ghana is in a jurisdiction with a long history of mining, and a stable political system," he said.

Cardinal expects a positive conversion to reserve from its upgraded Namdini resource

What helps set Cardinal apart is its strong management and development team who have extensive experience in Ghana and other African countries.

Koimtsidis is one of two board members who reside in Ghana, the other being executive director and Ghanaian citizen Malik Easah.

The board said the pair had extensive and well-established relationships locally and with the government, which significantly de-risked Cardinal's current and future operational presence.

Namdini's location also presents a lot of attractive advantages from a development and infrastructure point of view, Koimtsidis added, being located near all year round water, high voltage power grid and sealed roads to air and sea ports.

"Ghana also provides skilled labour through its extensive history of mining and the large number of operating mines in country," he said.

Looking ahead, the company expects to continue to generate positive news flow from its ongoing drill campaign on its greenfield exploration assets and the imminent PFS.

"Cardinal is continuing to deliver impressive results with its Namdini project development and shows encouraging regional exploration opportunities," Koimtsidis said.

He also pointed out the company's rapid rate of progress in Ghana.

"On average only half of all discoveries turn into operational mines," he said. "Of those deposits that are mined, there is a 12-year delay between discovery and development, on average.

"The lag time from a ‘discovery hole' to a ‘deposit' (initial resource calculation) is about 3 years. The conversion of a ‘discovery' to a ‘mine' is approximately 10 years for a gold mine.

"Cardinal is well ahead of this benchmark and is well-positioned to deliver a world-class, large scale gold mine with a long and sustainable life of mine, and in the process realise strong returns for our shareholders."